Argentina Citizenship by Investment and Tax Residency: Law 27.802 Confirms There Is No Automatic Tax Residency

The Labor Modernization Law No. 27.802, published in the Official Gazette on March 6, 2026, introduces a key clarification to Argentina’s Income Tax Law: there is no automatic tax residency, which directly benefits the Citizenship by Investment (CBI) framework currently in force in Argentina.

Argentina’s Labor Modernization Law No. 27.802, published in the Official Gazette on March 6, 2026, primarily focuses on reforms related to employment and labor regulations. However, Title XXIV (Amendments to Tax Laws), Chapter II, introduces a key clarification to Argentina’s Income Tax Law that directly benefits the country’s emerging Citizenship by Investment (CBI) framework.

This clarification is particularly relevant for investors and advisors analyzing the tax implications of Argentina’s citizenship by investment program.

The reform resolves an important concern frequently raised by international investors: obtaining Argentine citizenship through investment does not automatically create tax residency in Argentina.

Argentina’s Citizenship by Investment Program

Argentina introduced a framework for citizenship by investment through amendments to Citizenship Law No. 346, implemented by Decree 366/2025 (May 2025) and Decree 524/2025 (July 2025).

Under this regime, foreign nationals may obtain Argentine citizenship by naturalization without the traditional requirement of prior residence, provided they demonstrate relevant investments in the country.

Eligible investments are expected to focus on strategic productive sectors, including:

Energy

Technology

Agribusiness

Infrastructure

Real-economy investment projects

Applications are submitted to the Citizenship by Investment Program Agency, which operates under the Ministry of Economy and evaluates the investment projects before issuing recommendations to the National of Migration Agency.

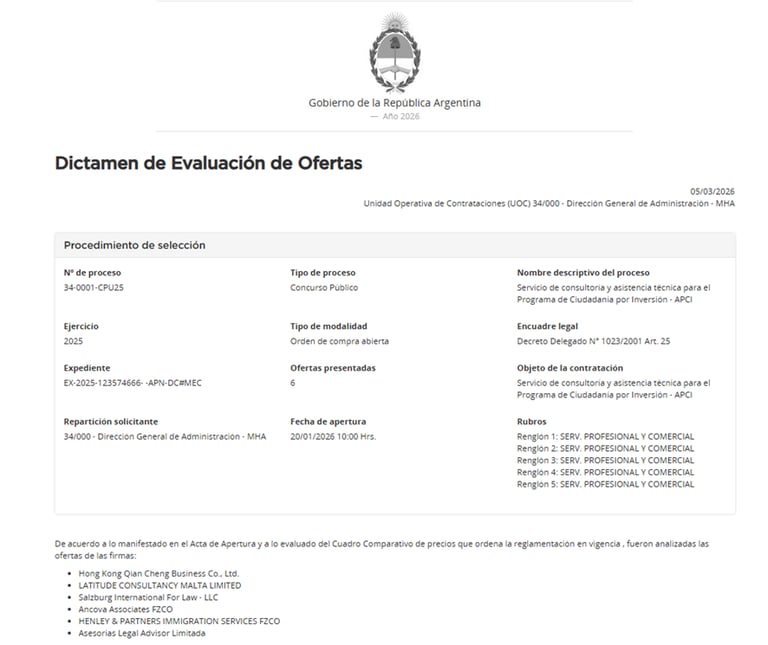

As of March 2026, the program is advancing through its implementation phase. The Argentine government conducted an international procurement process to select program operators, where out of six proposals received, only two met the formal requirements:

Henley & Partners Immigration Services FZCO

Asesorías Legal Advisor Limitada – UT Consorcio AAPA

The program is expected to become fully operational during the second half of 2026.

Based on preliminary estimates, minimum investments could be around USD 500,000 per applicant. Considering that the procurement process contemplates up to 5,000 potential cases, the program could attract approximately USD 2.5 billion in foreign direct investment.

Tax Implications of Argentina’s Citizenship by Investment Program

Article 194 of Law 27.802 introduced new paragraphs into Article 116 of Argentina’s Income Tax Law (2019 consolidated text).

The law expressly provides that:

“Foreign individuals who obtain Argentine citizenship by naturalization as a result of having made relevant investments in the country (…) shall not be considered tax residents (…) solely by reason of such naturalization.”

This means that citizenship obtained through investment does not automatically trigger tax residency in Argentina.

The reform clearly distinguishes two different legal concepts:

Nationality or citizenship, governed by constitutional and migration law

Tax residency, determined under specific tax rules

Foreign Tax Treatment for Investors

For purposes of applying Article 116(b) of the Income Tax Law, individuals who obtain citizenship through investment continue to be treated as foreign nationals when determining tax residency.

Therefore, the same criteria applicable to any foreign individual apply, including:

Physical presence in Argentina for more than 183 days during a calendar year

Establishment of a center of vital or economic interests in Argentina

Existence of relevant economic ties or permanent establishments

In other words, citizenship by investment alone does not activate Argentine tax residency.

Tax residency only arises if material connections with the country are established.

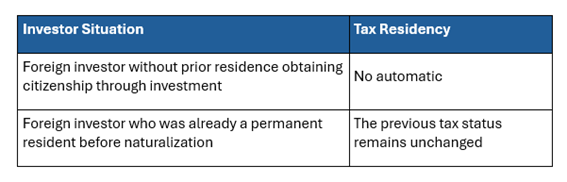

Exception: Investors Who Were Already Permanent Residents

The law also provides an explicit exception.

Individuals who already held permanent residence in Argentina at the time they obtained citizenship through investment will continue to be treated as Argentine tax residents.

In such cases, the naturalization process does not change their pre-existing tax status.

Practical Scenarios

Strategic Implications for International Investors

This clarification significantly strengthens the attractiveness of Argentina’s citizenship by investment framework.

In many jurisdictions, acquiring citizenship or residence may automatically trigger worldwide income taxation, which can discourage high-net-worth investors.

By contrast, Law 27.802 confirms that Argentine citizenship obtained through investment does not automatically result in global tax liability.

This approach provides investors with:

Greater certainty for international tax planning

Compatibility with double taxation treaties (Argentina maintains agreements with Spain, Germany, Switzerland, Italy and other countries)

Flexibility to structure cross-border investments

A Positive Signal for Foreign Investment

From a policy perspective, the reform sends a clear signal to international investors interested in developing projects in Argentina.

By separating citizenship from tax residency, the Argentine legal framework aligns with successful citizenship by investment programs in the Caribbean and Europe, prioritizing productive investment without imposing automatic tax consequences.

Legal Advice for International Investors

The evolving legal framework creates opportunities to structure investments combining:

Argentine citizenship

productive investment projects

international tax planning

Each case requires careful evaluation of:

the legal structure of the investment

qualification of the investment as “relevant” under the applicable regulations

the investor’s tax situation in their home jurisdiction

applicable double taxation treaties

potential risks of becoming a tax resident in Argentina.

For inquiries regarding Argentina’s citizenship by investment program, investment structuring, or international tax planning, please contact:

Aníbal Falivene

Attorney at Law | Argentina

More than 25 years advising international investors on cross-border investments, corporate structures, citizenship and residency by investment, and wealth planning.

Legal Advice

Protecting investors in stocks, bonds, cryptocurrencies, and other assets.

Attorney Aníbal Falivene

C.P.A.C.F. Registration: T. 71, F. 132

25 Years of Experience

I want to be contacted

Online verification:

Public Bar Association of the Federal Capital (Buenos Aires, AR)